The Federal Government announced a comprehensive reform to the Foreign Acquisitions and Takeovers Act 1975 (Cth) (FATA) on Friday 5 June 2020.

The reforms include measures to strengthen the existing framework with:

The COVID-19 temporary changes (announced on 29 March 2020) are not immediately affected. These temporary changes are set out at the end of this article.

The Federal Government will release exposure draft legislation in July ahead of a six week consultation period.

The reforms are scheduled to commence on 1 January 2021 and are supported by the Foreign Investment Review Board (FIRB).

Reasons for reform

Many countries have reviewed and updated their foreign investment regimes in recent years to manage new risks.

Australia also needs to respond to new risks and challenges.

The 2020 reforms package builds on reforms from 2015.

Underlying principles

The Federal Government sees that a balance is required between:

The Federal Government will continue to review individual investments on a case-by-case basis to ensure they are not contrary to the national interest. Conditions will continue to be attached to approvals on a case-by-case basis as the principal means of mitigation and safeguard.

Protecting Australia’s National Interest

Under the current regime (outside of the temporary changes introduced in response to COVID-19), foreign persons must seek government approval for investments above certain thresholds, dependent on the sector and country of the investor. Monetary thresholds mean investments in some sensitive sectors are not screened, even where an investment raises national security concerns.

A new national security test will be introduced for investments that raise national security concerns and which fall below existing monetary thresholds.

The new national security test will:

Investments subject to the new national security test will be assessed in relation to factors that give rise to national security concerns. Relevant factors may include:

(refer to the meaning of “security” in Australian Security Intelligence Organisation Act 1979 (Cth)).

National interest test

The existing national interest test will remain unchanged.

The national interest test takes into account:

To avoid overlap between the two tests, where the broader national interest test would apply to a particular action, only that test will be used in an assessment. This is because national security is already taken into account as a relevant factor of that test.

Where the national interest test applies, the Federal Government already considers national security in assessing a proposed investment. It is where the national interest test does not apply, but the investment raises national security concerns, that the new national security test will enable the Federal Government to review investments which would ordinarily be exempt from screening.

Sensitive national security business

A new definition of sensitive national security business for mandatory notification will be introduced in regulations. This is consistent with the approach for defining sensitive businesses and allows the definition to be adapted over time.

The definition of sensitive businesses includes media, transport, telecommunication businesses, and businesses providing infrastructure to these businesses (s 22 FATA) is considered by Treasury to be too broad for the new mandatory notification requirements.

There will be consultation in relation to the new definition of sensitive national security business alongside release of the exposure draft legislation, which will explore concepts including:

‘Call in’ power

The proposed legislation will create a new power to “call in” investments on a case by case basis (before, during or after investment) where the Treasurer considers the investment raises national security concerns. The Treasurer will also be able to review the investment under the national security test.

Public guidance will be issued as to the type of investment where the “call in” power could be used.

Voluntary notification

Investors will also have the opportunity to voluntarily notify FIRB, to avoid the possibility of a proposed acquisition being “called in” for review on national security grounds.

Where a voluntary notification occurs for an investment that is not subject to mandatory notification, a time-limited period will commence in which the Treasurer will need to decide whether to exercise the “call in” power and review the investment on national security grounds.

It will be interesting to see how the amending legislation will deal with a situation such as where a defence installation is subsequently established next to land that has already been acquired by a foreign entity.

Investor-specific exemption certificates

Investors will be able to apply for time-limited investor-specific exemption certificates (that will be subject to conditions, such as reporting) which will enable investors to make eligible acquisitions without case by case screening. This will reduce the regulatory burden of making separate applications, with resultant time and cost savings.

National security last resort review power

A new national security last resort review power will be introduced, to allow approved foreign investments to be re-assessed where subsequent national security risks emerge.

This power is intended to address a gap where point-in-time approvals, including conditions, may be made redundant due to rapid technological change or where security risks change post approval having been given.

Where there are no other regulatory mechanisms to satisfactorily address national security risks, the Treasurer will be able to impose conditions, vary existing conditions, or as a last resort, require the divestment of foreign interests. The Treasurer will need to substantiate that subsequent to the original approval:

This power will not be retrospective – this power will only apply to a foreign investment made after this power is that is created.

The power will be subject to significant safeguards – reflecting the need for investor certainty and transparency. The devil will be in the detail with respect to this aspect of this power. The real concern with this power is that it elevates the sovereign risk issue for foreign investors.

Streamline less sensitive investments – exemption of certain investments

Certain investments made by entities which are currently classified as “Foreign Government Investors” (FGIs) will be exempt.

Currently the definition of FGI is broad and includes foreign governments and their agencies, and includes corporations, trustees of trusts and general partners of limited partnerships in which:

If an investor is considered an FGI, foreign investment approval is required for a range of transactions which would not be required if the investor was a private investor.

The reforms mean that some investment funds (with investors who are FGI’s) will no longer be treated as FGIs where it can be shown that the FGI investors have no influence or control over the investment or operational decisions of the entity or any of its underlying assets.

Entities which have more than 40% foreign government ownership in aggregate (without influence or control) but less than 20% from any single government will no longer be deemed to be an FGI under the Foreign Acquisitions and Takeovers Regulation 2015 (Cth) (FATR).

Entities which have a single foreign government with at least 20% ownership (without influence or control) will still be deemed to be FGIs. However, they will be able to apply for a broad exemption certificate on a case by case basis.

These entities would still be subject to screening at thresholds for private foreign investors, and the new national security test will apply if the investment raises national security concerns, regardless of value of investment.

Stronger penalties, compliance and enforcement powers

The reforms will ensure that the Treasury and the Australian Taxation Office (ATO) have more effective resources, powers and penalties to effectively monitor, investigate and prosecute breaches of foreign investment laws.

Standard monitoring and investigative powers:

Currently, Treasury relies on the general information gathering power under s 133 of the FATA to monitor and investigate non-compliance and the ATO uses powers under the Taxation Administration Act (1953) (Cth) (TAA).

The existing information gathering power is sometimes insufficient to assess compliance, e.g. in relation to conditions requiring installation or removal of surveillance or communications equipment. The FATA provides for desk-top and paper-based auditing and compliance monitoring but does not provide for site or site-based inspections or investigations.

The reforms will provide standard monitoring and investigative powers (in line with those of other business regulators), including access to premises with consent or by warrant to gather information.

This will improve the regulators’ capability to monitor investor compliance and/or investigate potential non-compliance.

Powers will likely be obtained by triggering the Regulatory Powers (Standard Provisions) Act 2014 (Cth).

The ATO would continue to access powers under the TAA.

Obtain directions power:

Currently, there is no directions power under the FATA, so the Federal Government is not able to pursue early and effective action to remedy a breach of conditions.

The reforms will provide the Federal Government with powers to give directions to investors in order to prevent or address suspected breaches of conditions of the foreign investment laws.

There would have to be a ‘reason to suspect’ that an investor has, is, or will, engage in conduct that breaches a condition of their approval or breaches a foreign investment law for the directions power to be triggered.

An investor will be required to comply with a direction. Failure to comply will expose the investor to enforcement mechanisms.

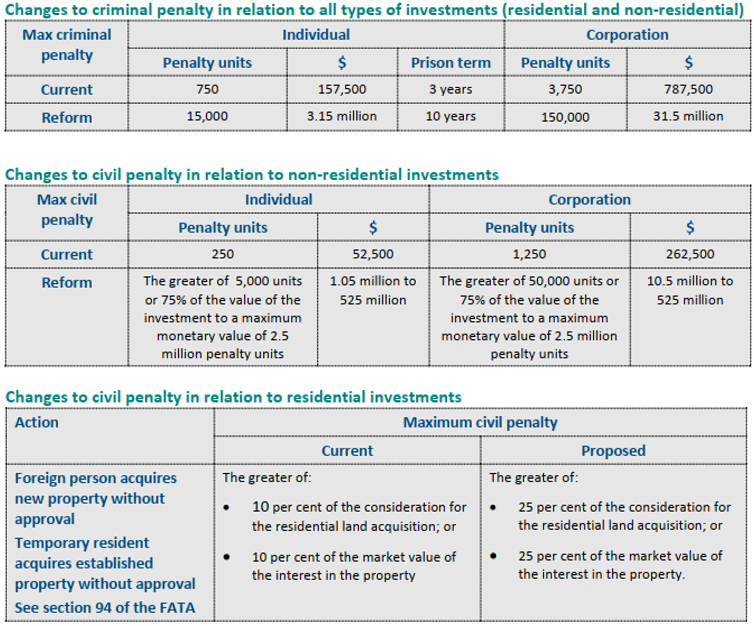

Increase civil and criminal penalties:

Current monetary penalties under the FATA are low compared to other business regulatory regimes and do not provide a meaningful deterrent against non-compliance.

The reforms will increase civil and criminal penalties under the FATA to ensure the penalties act as an effective deterrent.

*Tables extracted from the Treasury’s summary booklet on Foreign investment reforms, June 2020.

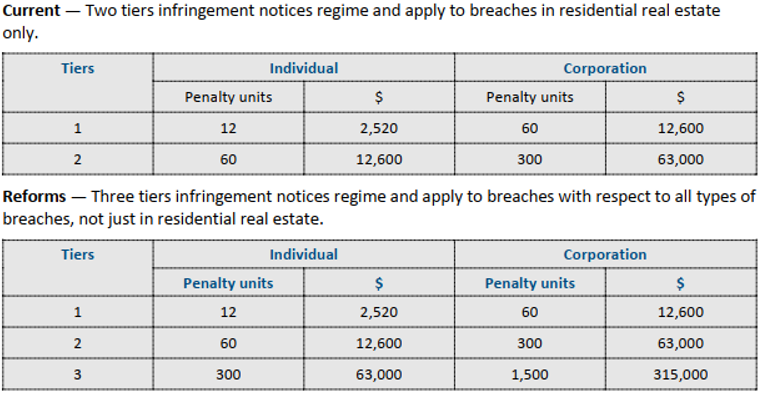

Expansion of the infringement notices regime:

Currently, FATA allows less serious breaches of foreign investment rules to be punishable by infringement notices.

This is limited to residential real estate investment.

The Federal Government will expand the infringement notices regime to cover all types of foreign investments and introduce a third tier to allow for a more graduated and proportional approach to enforcement.

Currently, there are two tiers in the infringement notices regime. The lower level Tier 1 penalties apply if the person self discloses the conduct that gives rise to the penalty. The higher Tier 2 applies in all other cases.

The reforms will introduce Tier 3 for non-compliance in relation to high-value acquisitions (e.g. above $5 million).

Infringement notices will attach to business investments.

*Tables extracted from the Treasury’s summary booklet on Foreign investment reforms, June 2020.

Powers to remedy incorrect statements

Currently, there are no specific provisions that allow for adequate remedy if a person makes an incorrect statement or omits an important piece of information when notifying the Federal Government of a proposed investment and which the Federal Government relies on (other than the anti-avoidance rules under s 78 of the FATA).

Under the reforms, the government will have powers to remedy situations where foreign persons are given a no objection notification, or an exemption certificate based on a foreign investment application that makes an incorrect statement or omits an important piece of information.

The reforms will include:

Strengthen the Federal Government’s powers with respect to an interest transferred by will or devolution by operation of law

Currently s 29 of FATR provides broad exemption in respect of interest acquired by will or devolution by operation of law. Exemption applies even where original acquisition was not notified to Federal Government in breach of FATA.

The amendments will:

Power to accept enforceable undertakings

The legislation will give the Federal Government the power to accept enforceable undertakings from foreign persons to manage non-compliance or to give weight to commitments a foreign person made at the time of applying for a no objection notification or an exemption certificate.

Enforceable undertakings will provide an effective deterrence regime, providing a mechanism to prevent actions which could place the national interest at risk and restore compliance without recourse to court action.

Enforceable undertakings would be available where:

Notification that an action has been taken

It is often difficult to enforce conditions that only take effect upon the action occurring, because Treasury is not aware when these conditions take effect.

A requirement will be introduced that foreign persons who have been issued a no objection notification for a proposed action or an exemption certificate, will be required to notify the Federal Government of certain events, including that the action has occurred, or did not occur, within a specified number of days.

Integrity of the investment review framework

Improve the integrity of the approval process

Foreign persons will be required to seek further foreign investment approval for any increase in actual or proportional holdings above what has been previously approved, including as a result of creep acquisitions and proportional increases through share buybacks and selective capital reductions.

Changes in control above 20% and increases in interests in entities above 20% as a result of a share buyback or selective capital reductions will require approval.

Narrow the scope of the moneylending exemption

Section 27 of the FATR currently exempts for all purposes, the acquisition of an interest in securities, assets, a trust, Australian land or a tenement if the interest is held solely by way of security for the purposes of a moneylending agreement.

The amendments will narrow the scope of the moneylending exemption so that it does not apply where foreign money lenders are obtaining interests in a sensitive national security business under a moneylending agreement.

Approval will be required before obtaining interests in a sensitive national security business.

Oversight of Commonwealth, state, territory and local government asset sales

Foreign persons will be required to seek foreign investment approval for acquisitions of interests from the Commonwealth, State or Territory governments or local government bodies to perform government services or functions associated with privatisation programs that may raise national security risks.

Currently section 31 of the FATR exempts certain acquisitions from Australian governments from the FATA, except for acquisitions by foreign government investors or acquisitions of specified infrastructure from Australian governments (or ‘Australian businesses’ holding interests in such infrastructure).

The proposed amendments will ensure that the Federal Government has the opportunity to review and determine that proposed investments into a service, function or asset from a government entity are not contrary to national security.

Extend the tracing rules to apply to limited partnerships

The FATA will be amended so that the tracing rules under section 19 of the FATA can be similarly applied to unincorporated limited partnerships as they are to corporations and trusts, so that beneficial interests can be traced.

Prevent the use of family structures to subvert the operation of the FATA

A foreign person, who is a parent or spouse of an Australian resident, will need to seek foreign investment approval prior to the purchase of Australian land where they provide money to their Australian family member for the purchase.

The amendments will cover situations where a foreign family member provides money to an Australian family member, and a trust or equitable interest in the property arises in favour of the foreign family member.

The “presumption of advancement” (a common law principle that, in certain circumstances, where a person purchases property in the name of another person, they intended to make a gift to that other person) will be excluded from the FATA.

An exemption may apply where it can be shown that money provided by the foreign family member was a genuine gift.

More coordinated information gathering and sharing

A new Register of Foreign Ownership

The Federal Government is considering a new “Register of Foreign Ownership” that will merge and expand the existing agricultural land, water and residential registers.

The Register of Foreign Ownership will be administered by the ATO.

The aim is to increase the Federal Government’s visibility of foreign investments made in Australia. The information gathered on the register would be shared across government, subject to appropriate safeguards.

The Register of Foreign Ownership will not be able to be searched by the public due to commercial sensitivities and privacy considerations.

Greater sharing of foreign investment information

The scope of the information sharing provisions under the FATA and the Tax Administration Act 1953 (Cth) will be increased to allow greater sharing of foreign investment information across government agencies to simplify the administration of the foreign investment framework.

Amendments and new information sharing provisions will be introduced, subject to appropriate safeguards, to enable sharing of protected information, between ATO and FIRB (rather than through Treasury as currently required), as well as with international counterparts in limited circumstances where national security considerations are present.

A fairer and simpler framework for foreign investment fees

Presently, fees are generally payable by a foreign person who makes an application under the FATA and applications are only considered once the correct fee has been paid.

The Federal Government maintains that Australian taxpayers should not bear the cost of administering the foreign investment review framework.

Accordingly, the fee schedule will be updated to ensure they continue to cover the costs of administering the system. This includes reflecting the enlarged roles and responsibilities of foreign investment activities across government, and the administrative cost of the review process over recent years.

The Federal Government is also committed to reforming the fees framework to make it fairer and simpler for investors. The updated fee schedule will be fairer and simpler to reduce complexity and compliance costs for foreign investors.

A timely, consistent and reliable investor experience

The Federal Government is committed to delivering a timely and efficient foreign investment regime which recognises commercial deadlines and does not unnecessarily impede the operation of foreign investors or markets. The Federal Government will continue to work with stakeholders in identifying ways to streamline and enhance the investor experience.

Other technical amendments

The Federal Government will introduce amendments to the foreign investment review framework to improve the readability of existing provisions, rectify inconsistencies and unintended consequences, and address feedback from investors seeking greater certainty.

Amendments include:

***

COVID-19 Temporary Changes

Temporary changes to foreign investment framework in response to COVID-19 were announced in March.

The following changes took effect from 10:30pm AEDT, 29 March 2020 (Effective Date):